South Florida Events – July 2025

Check out the local South Florida events in July, including the Key West Key Lime Festival, FlockFest and the South Florida Wing Bash.

Check out the local South Florida events in July, including the Key West Key Lime Festival, FlockFest and the South Florida Wing Bash.

The Florida Association of REALTORS has updated their standard listing agreement to provide sellers with 3 options for compensating brokers.

Our Favorite New Condominium Projects in the Fort Lauderdale Area Demand is still high for new construction condos in the Fort Lauderdale area, and developers are delivering. The following projects

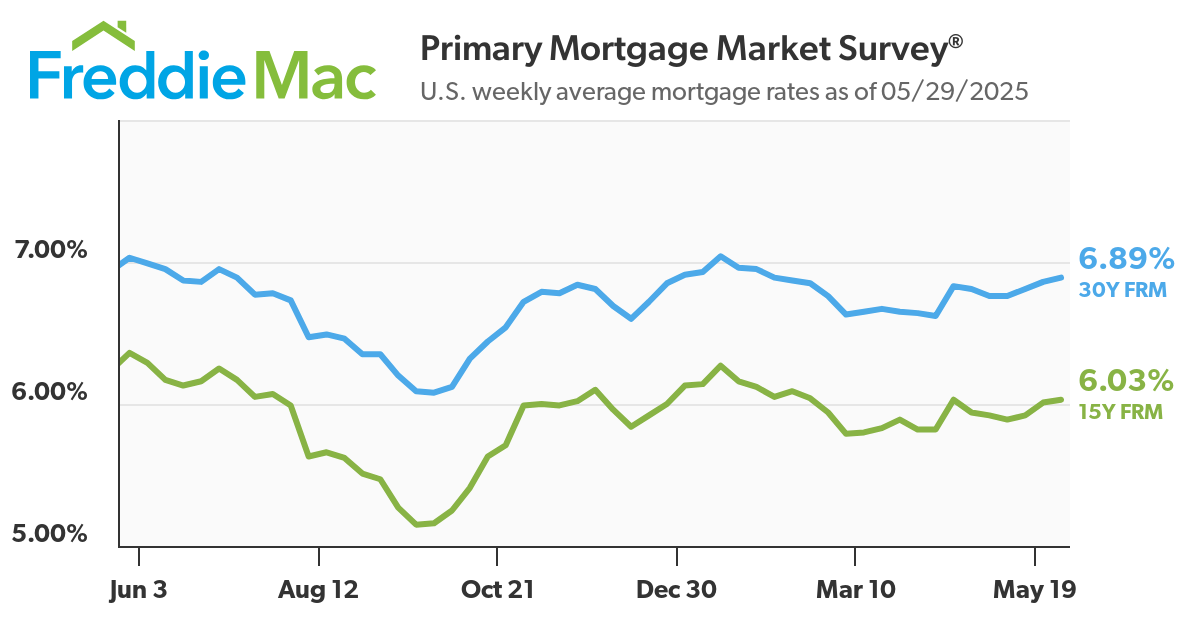

The 30 year fixed rate mortgage has bounced around between 6% and 7% for past year and will likely continue this way for some time. Active buyers and their lenders should follow rates closely and lock in to take advantage of the declines when they happen.

Check out the local South Florida events in June, including The Hukilau, Scuba4Good Music Fest and the Summer Fruit Festival.

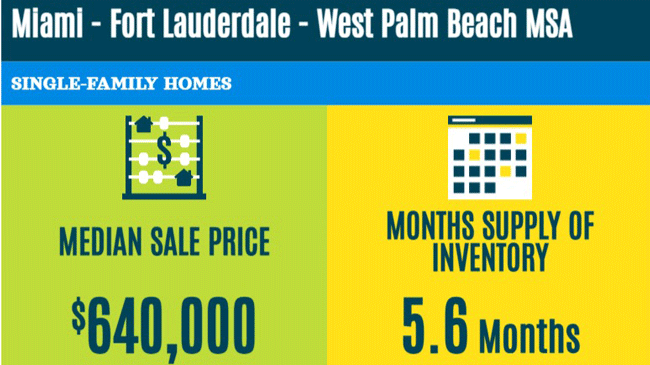

Inventory levels on Fort Lauderdale’s waterfront are technically favoring buyers, but we still wouldn’t call it a buyer’s market. Check out the October reports.

2 years ago we had less than 6 months of oceanfront condo inventory in Northeast Broward County. We now have 13 months of supply and arguably a strong buyer’s market.

Check out the local South Florida events in May, including the Miami Grand Prix, Fort Lauderdale Air Show and The Great American Beach Party

Check out the local South Florida events in April, including the Tortuga Music Festival, Delray Affair and the Las Olas Wine and Food Festival

Buyers are getting comfortable with older condo buildings and as a result they are getting some amazing deals. Condos are now selling at 92.7% of list price, the lowest list to sell ratio in 13 years.

Swordfish can be caught year round in South Florida and fresh swordfish is readily available in most local seafood markets and supermarkets. Fresh fish is always best on the grill,

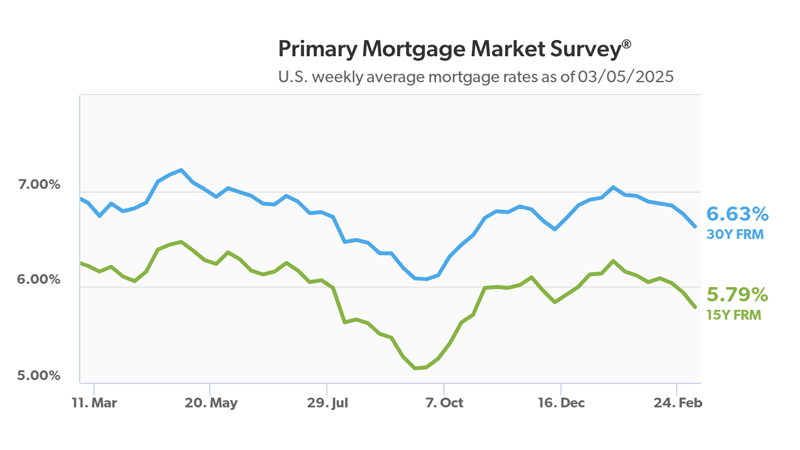

The 30 year fixed rate saw its largest decline since last September. Most analysts believe the 30 year rate will bounce around between 6 and 7% for the near future.